Editor’s choice

Editor’s choice

Achieving net-zero emissions by 2050 – which is, after all, what is needed to give us a good chance of not exceeding 1.5°C – requires the decarbonization of industry. Not by some, but by all. There’s no free ride to 1.5.

This article is based on remarks made at the Climate Action Summit on 22 September. It draws on the input of SEI researchers Björn Nykvist and Aaron Maltais.

I want to hear about how we are going to stop the increase in emissions by 2020, and dramatically reduce emissions to reach net-zero emissions by mid-century.

UN Secretary-General António Guterres

Technologically, reaching net-zero emissions in industrial sectors is possible. Carbon capture and storage, electrified industrial processes, biomass, hydrogen and synthetic fuels from renewable electricity are all, in theory, technically possible today and, taken together, would mitigate these emissions.

But what will unleash these technologies, everywhere and at scale? Three classes of innovation: policy, technology and finance.

In absolute numbers globally, the costs associated with decarbonizing industry and heavy road transport are staggering. But the amount of needed investments would have only a small impact on the overall economy, with cost estimates in the range of 0.5% to 1% of global GDP.

However, for individual companies looking to decarbonize, production costs could in some cases actually double. Passing these costs on to buyers can look very challenging, especially for sectors exposed to international competition and markets. When companies do not clearly see how they can charge their customers for the costs of decarbonization, they will not make the needed investments – even if the additional cost on final products at the end of the supply chain is small.

The key nut to crack, then, is how to distribute that cost and how to share the risk among the private and the public sectors.

The appetite for investment vehicles is large – green bonds always find investors, who often demand more of them than are available. But the problem is that, as a whole, the financial sector (and some companies too) continue to assess risks and rewards in traditional ways. Long-term climate risks are not factored in unless policies are in sight to raise carbon prices or ban fossil fuels. Innovative solutions that have not yet been developed at scale are assessed as inherently riskier. The EU taxonomy for green bonds is a good start in determining the good and the bad for green bonds. Such an approach could be extended to other financial instruments.

Major innovations are still needed to scale-up the technologies needed to mitigate industrial emissions. Engineers will have to re-think numerous industrial processes, figuring out how renewable fuels, or renewable electricity, can replace fossil fuels. Research on producing, storing and distributing hydrogen to enable wider deployment across the economy is still at a relatively early stage. And we are still working out how to produce biomass sustainably so that it can become a feedstock for the chemicals industry and for biofuels (let alone the challenge of building large scale biorefineries that produce the polymers for a huge range of products). Bearing this in mind, the state needs to support demonstration and deployment, where investment costs become really significant.

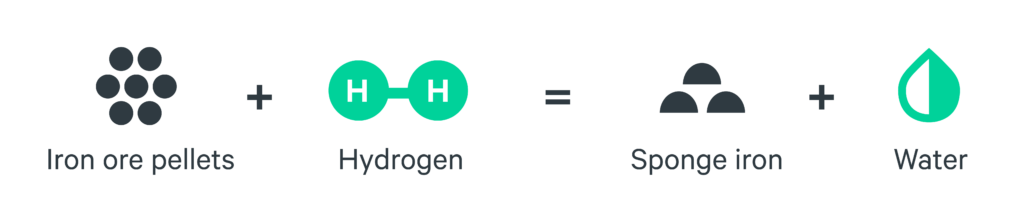

Iron reduction based on hydrogen. One of the technological innovations that needs to be scaled up. Image: HYBRIT (adapted)

Governments need to provide incentives for companies to decarbonize, and decarbonize quickly. Sufficiently high carbon taxes covering most regions and sectors would change the competitive landscape, not only creating an incentive to invest in decarbonization but also ensuring low-carbon technologies are not at a price disadvantage. But with no higher carbon price in sight, any company that wants to decarbonize has to invest large amounts of capital over a very long time, while still being exposed to international competition. Governments need to start playing a bigger role in providing financing to companies that are ready to pilot and demonstrate carbon-neutral solutions.

Expanding industry policy like this is already natural to many countries. One policy tool that seems to have been effective in Sweden is sectoral roadmaps. Based on the decision by the parliament to make Sweden climate neutral by 2045, the Fossil Free Sweden initiative has encouraged business sectors to draw up their own sectoral roadmaps to be fossil free while increasing competitiveness. The roadmaps may be sectoral, but they have also added value in three other ways:

These roadmaps show where sectoral measures intersect and where there is the potential for new markets, jobs and prosperity. The hope, and emerging evidence, is that these partnerships – and others – can catalyse the net-zero transition within, and across, industries.

Such public-private-partnerships are possible in many other countries. Governments could aid this process further by guaranteeing markets. Setting rules for public procurement that require low-carbon cement or low-carbon steel in publicly funded infrastructure is one example of how governments could help to guarantee future demand.

Scaling up industry transitions is a winning concept. Reaching critical mass will unlock major value and de-risking, but will need the support of international policy (e.g. on intellectual property, technology transfer), standards (e.g. “green steel”) and finance. Coalitions of countries and companies are already setting out on collaborative journeys to net-zero. What we need now are the industry transition roadmaps that lead to the value chains of tomorrow.

Here are three overarching considerations for industry transition roadmaps to succeed:

The challenge after the Climate Action Summit is to translate plans and initiatives into specific actions, to connect these to the implementation of the Paris Agreement and 2030 Agenda, and integrate them into countries’ broader development agendas. Industry transitions must be accompanied by rapid mobilization and scale-up of finance and innovation. The opportunity is enormous: the equation net-zero emissions + SDGs = a huge purchase order. It’s time to deliver.

Feature / Getting out of coal to reduce emissions is the order of the day but doing so is complicated. Here are five lessons from our research.

Other publication / With increased climate ambition, coal, oil, and gas production will need to wind down.

SEI working paper / Three Swedish companies plan to implement fossil-free steel production. Understanding these key factors will help make this ambitious plan a reality.