Editor’s choice

Editor’s choice

The US stepping in to offset European reliance on Russian liquefied natural gas may seem counterintuitive to advancing climate goals, but they can work in tandem, says SEI Senior Scientist Peter Erickson.

On 25 March 2022, the US and the EU announced a partnership to help Europe get off Russian natural gas. This move would both punish Russia for invading Ukraine and protect the EU from the possibility that Russia may restrict gas flows to the continent. Under the new program, Europe would reduce its demand for Russian gas by up to two-thirds, while the US would help make up the remainder by supplying about 50 billion cubic metres (bcm) of natural gas annually over the next few years to the EU.

Where will this new gas come from? If the US simply shifts existing liquefied natural gas (LNG) supply from other buyers to EU buyers, it could trigger even further supply shortages and price spikes in the global LNG market, which is already under-supplied. Prices at the import hub in the Netherlands have averaged about $30 per million British thermal units (MMBtu) in recent months, more than five times higher than pre-pandemic levels.

What is the US to do? The White House has committed to supply Europe with this large quantity of gas, not only in a way that helps bring prices down (not up), but also in a way “that is consistent with our shared net-zero goals” for reducing greenhouse gas (GHG) emissions.

Thankfully, the way to balance these objectives is not as difficult as it might appear, for three reasons:

First, the logistics of getting 50 bcm of LNG to Europe do not appear to require new infrastructure. US LNG exports to EU countries have already been ramping up rapidly (Figure 1) and align with the rapid expansion of US LNG export capacity.

US LNG shipments to Europe have been increasing dramatically.

Source: SEI analysis of US Department of Energy data.

Export rates will continue to increase such that attaining exports of 50 bcm is nearly assured (in fact, exports in January 2022 were already proceeding at that rate, even before Russia invaded Ukraine). Still, there is some question as to what the base year is for measuring the announced 50 bcm increase (meaning a 50 bcm increase relative to what?). The near-term plan – for an added 15 bcm in 2022 – can be met with already-planned expansion of US LNG capacity by about 25 bcm this year (as compared to 2021, thus making the US the world’s largest LNG exporter). Beyond 2022, and assuming the 50 bcm increase is meant to be relative either to to 2020 (as in one analysis) or to 2021, total annual US LNG exports to EU countries would to reach about 70 bcm. Even then, the 25 bcm of new capacity coming online by end of 2022, and yet another 25 bcm of new US export capacity under construction and online by 2025, suggests there should be no additional need for new LNG export terminals to supply a total of 50 to 70 bcm of LNG to Europe. In any case, additional not-already-under-construction export terminals would take too long to develop anyway, potentially locking in gas supply long past when it is needed. On the import side, Europe also has spare capacity, though that may need to be routed through the UK given intra-EU pipeline constraints.

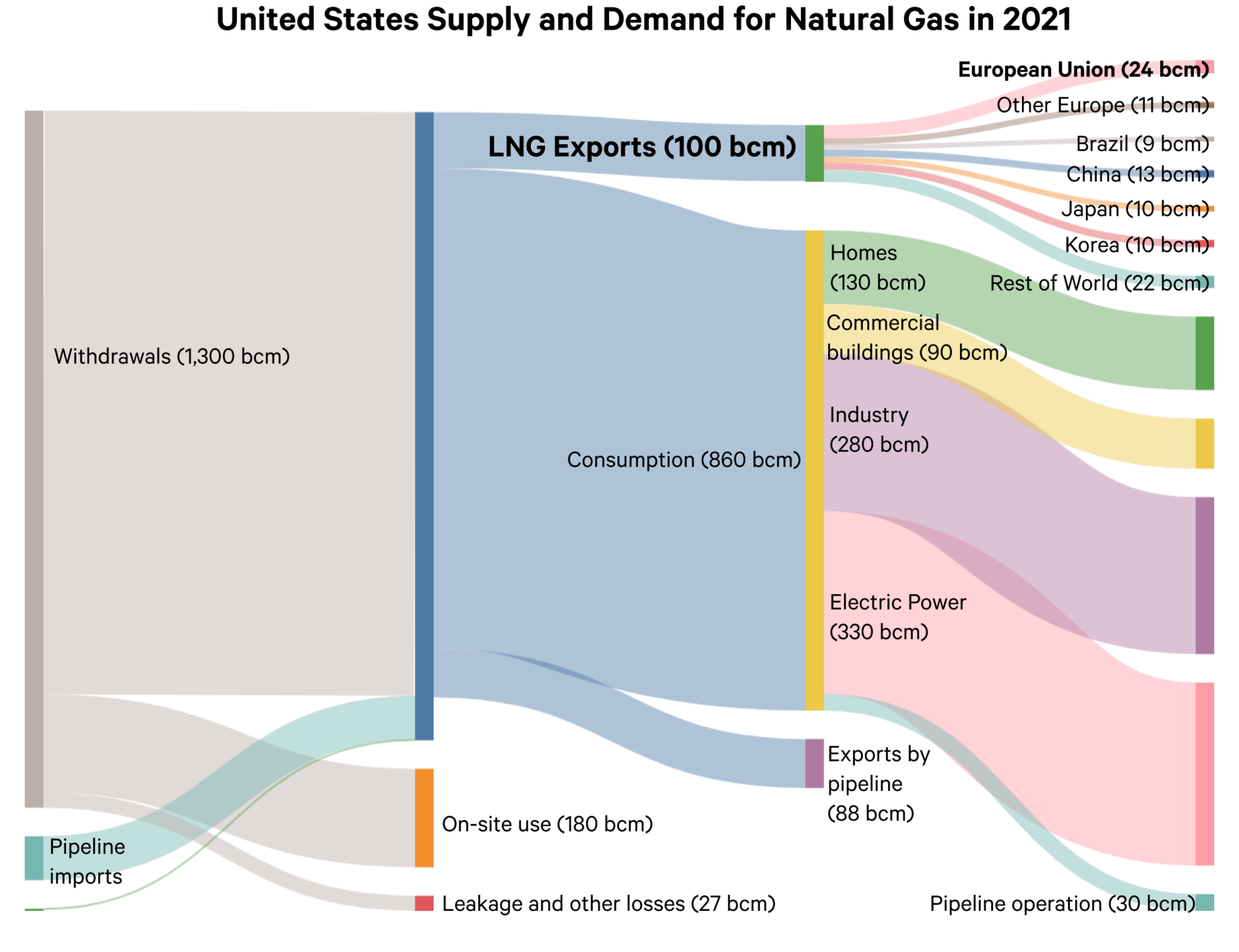

Second, there are ample ways for US policymakers to free up gas supply to Europe while advancing the US commitment to reduce greenhouse gas emissions. For example, as the recent Net-Zero America study found, an aggressive push towards clean energy and electrification in the US could reduce gas demand in the US by 30 bcm (or more) each year, which would free up plenty of gas to allow an added 50 bcm of gas annually to Europe, while simultaneously accelerating US energy security by speeding up the transition away from fossil fuels. Since current US gas demand is nearly 900 bcm annually, there are ample opportunities to make reductions both big and small in the power sector (renewables), building sector (heat pumps), and industry (efficiency; Figure 2). Furthermore, about 27 bcm of gas are simply lost in the US each year through leaks, venting and other losses (even more is flared) – much of it in Texas and other Gulf states in the vicinity of the LNG export terminals. Rapidly implementing practices to reduce flaring, leaks and venting of methane at oil and gas extraction sites could be a terrific way to reduce GHG (methane is 30 times more potent than CO2, ton for ton) plus other emissions, while rounding up a new source of gas to send to Europe. These examples show how it is possible to free up new supply without opening major new oil or gas developments (even as there may still be a limited role for some new, short-cycle investments in shale gas).

Third, the US should do everything it can to help the other buyers of its LNG reduce demand for gas. This especially applies to lower-income countries that buy its LNG, such as Bangladesh, India, Indonesia and Pakistan, but could also apply to facilitating trade and investment in middle-income countries that buy even more LNG from the US, such as Brazil, Chile, and China. The key is to reduce gas demand by building renewables and implementing efficiency instead of using more coal. Supporting the lower-income countries financially in a move to renewables would also help the US fulfill and expand its commitments to climate finance under the Paris Agreement. For example, building new solar and wind power facilities to replace the equivalent amount of electricity generated by the 8 bcm of gas sent to Bangladesh, India, Indonesia and Pakistan would cost only about $5 billion in capital costs which, spread over several years, would be a only a modest addition to the current US plan to provide $24 billion per year in climate finance.

Importantly, these efforts to reduce US and international demand for gas will help not only the climate, but also help bring about “the stability of supply and demand” sought by the US and EU, since the actions would also reduce LNG prices and volatility. Reducing gas demand is the fastest way to bring down prices in international LNG markets (faster than bringing on new supply, which can take many years). This would have important benefits for global equity, too, since consumers in the LNG-dependent countries would no longer be paying exorbitant rates for natural gas.

In summary, expanding US natural gas supply to Europe is a crucial step for maintaining energy security in Europe, and it need not conflict with climate goals. Instead, the US can free up new supply at home by rapidly reducing its own demand, by following through on existing plans (such as the stalled Build Back Better Act) to advance renewable power, building electrification, and reduction of methane loss at oil and gas infrastructure. Further, the US can help reduce gas demand in the countries that buy its LNG.

Meeting global climate goals, such as holding warming to 1.5° or 2°C, necessitates a long-term move away from fossil fuel consumption and production. Thankfully, that still leaves room for shorter-term opportunities to manage gas supply (and demand) in strategic ways.

Natural gas flows in the United States in 2021, measured in billions of cubic metres (bcm). Given US gas consumption of over 860 bcm, there are ample opportunities to free up 50 bcm for the EU.

Source: SEI analysis based on data from the US Department of Energy. Methane losses estimated at 2.3% of production, per Alvarez et al. 2018.

Initiative / The Carbon Lock-In Initiative seeks to uncover and address the barriers that uphold the fossil fuel-based economy.

Perspective / As we decarbonize our energy system, we must also address the harmful public health and environmental impacts of oil and gas extraction.

Other publication / The 2021 report reveals that countries' fossil fuel production plans remain dangerously out of sync with the limits consistent with the Paris Agreement.

Feature / Citing climate change concerns, a United States federal judge used SEI research on greenhouse gas emissions to halt Gulf of Mexico oil and gas leases.